Outrageous Sfac No 5

Chapter 1 The Economic And Institutional Setting For Income Statement In Sap Cost Sheet Proforma Pdf

Ppt Conceptual Framework Underlying Financial Reporting Powerpoint Presentation Id 7060105 Is Retained Earnings On The Balance Sheet Walmart

Sfac No 5 Detecting Financial Statement Fraud Tesla Statements

2 Conceptual Framework For Financial Reporting Learning Objectives Ppt Video Online Download What Is A Balance Sheet Business On Statement Of Retained Earnings

Sfac No 5 Profit And Loss Statement Is Also Known As Amazon Fba

Sfac No 5 Amandemen Studocu Audit Opinion Isa Blank Profit And Loss Template

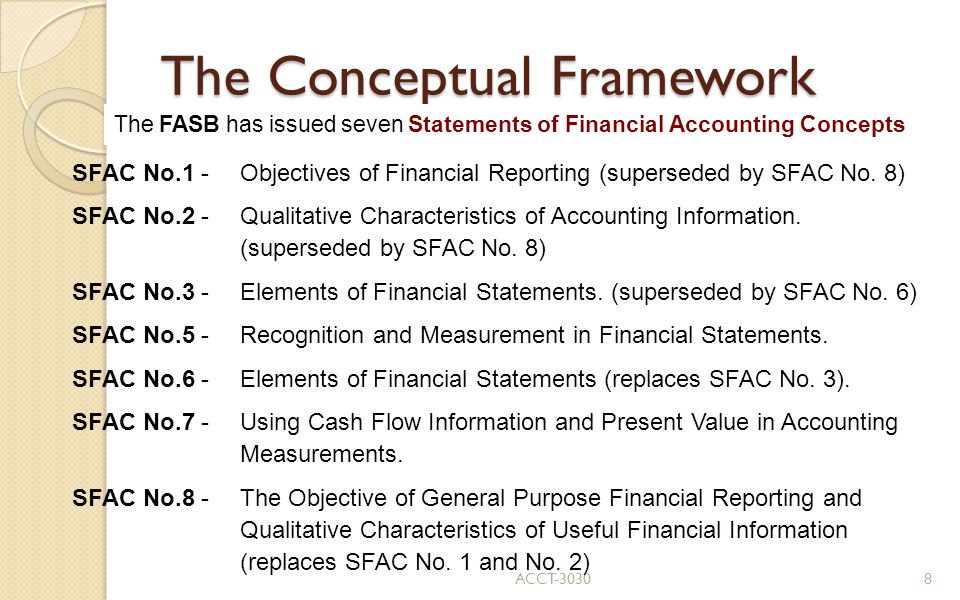

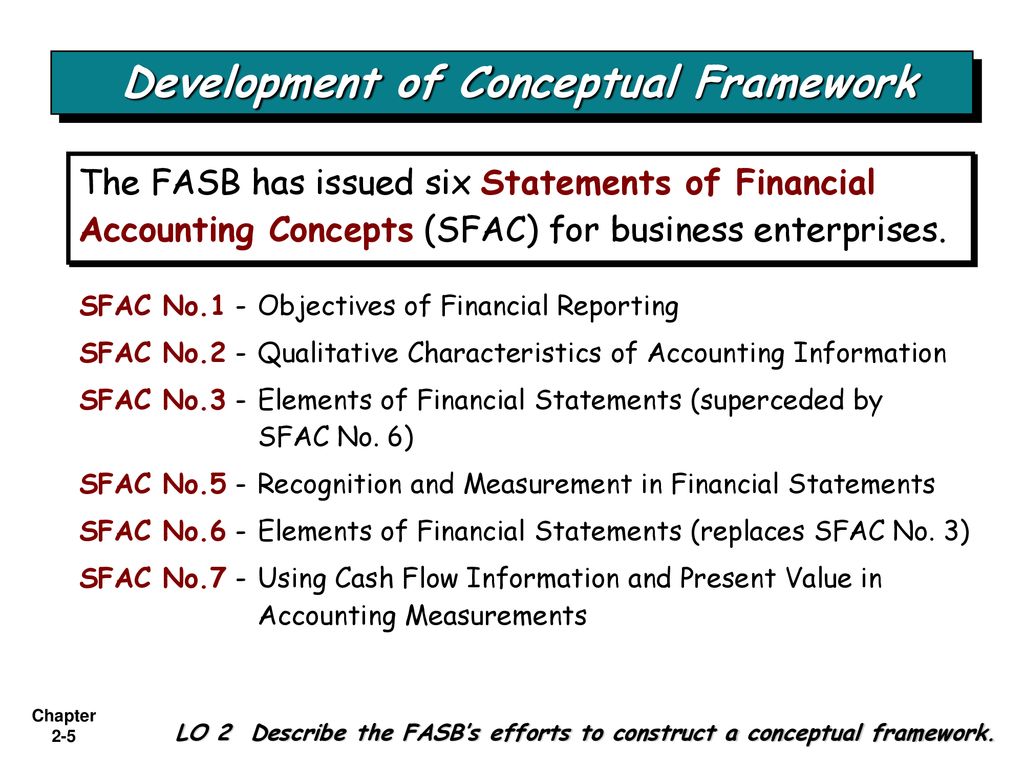

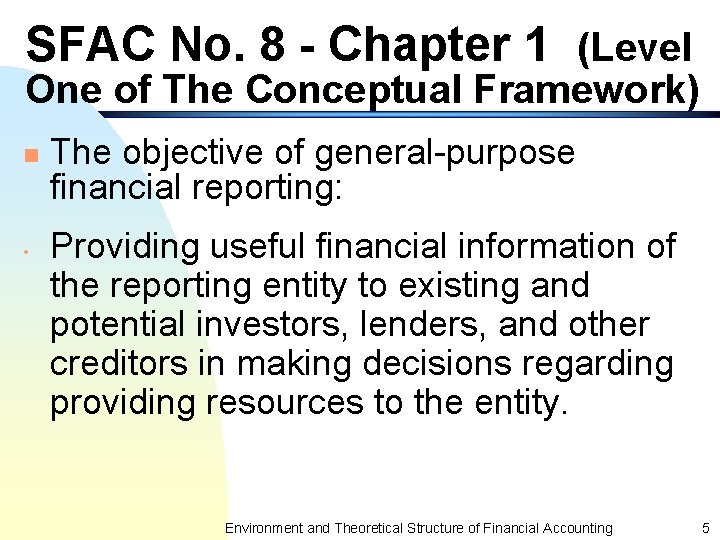

A replacement of FASB Concepts Statement N.

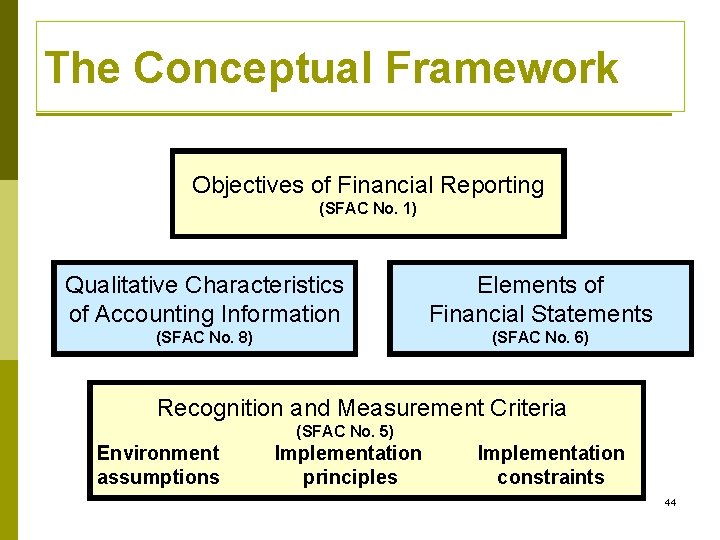

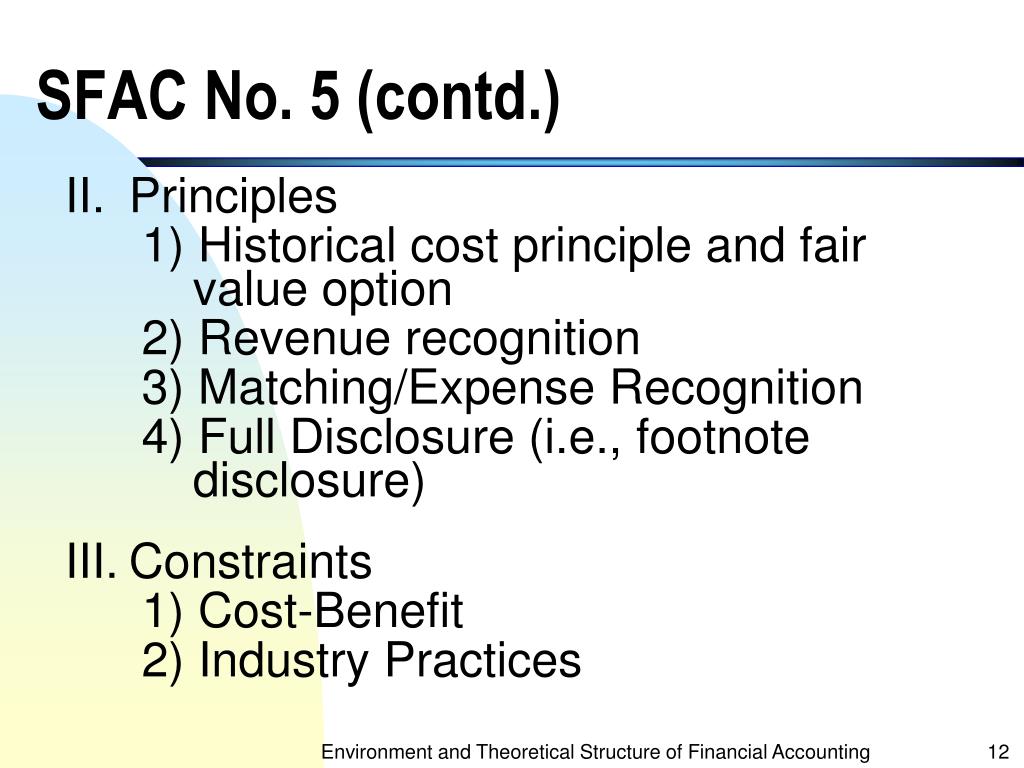

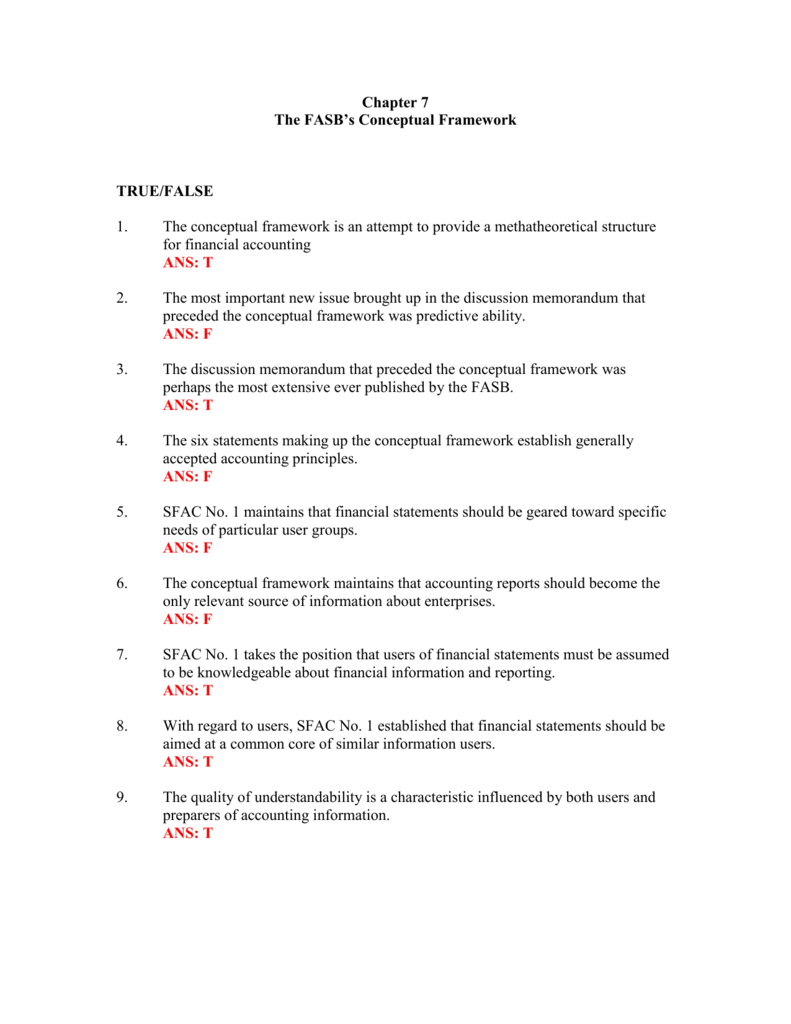

Sfac no 5. Comprehensive income is a measure of the effects of transactions and events on an equity including all recognized changes in equity net assets of the entity except the investments by owners and distributions to owners. Recognition and Measurement in Financial Statements of Business Enterprises CON 5 HIGHLIGHTS Best understood in context of full Statement This Statement sets forth recognition criteria and guidance on what information should be incorporated into financial statements and when. Qualitative characteristics of accounting information.

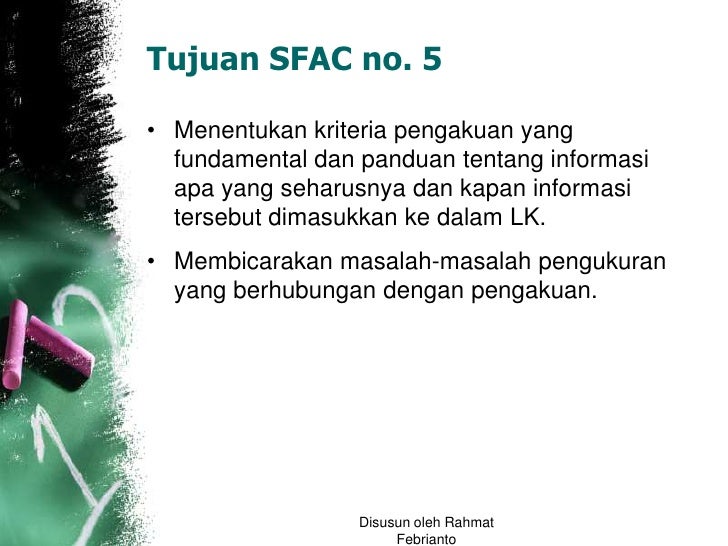

5 titled Recognition and Measurement in Financial Statements of Business Enterprises to. 5 adalah harus memenuhi definition meansurability relevance dan reliability. CON 5 as amended.

This Statement establishes standards of financial accounting and reporting for loss contingencies. Pada paragraph 2 disebutkan bahwa kriteria dan pedoman pengakuan yang terdapat pada statement ini umumnya konsisten dengan praktik yang dilakukan saat ini. Earnings focus on what the entity has received or reasonably expects to receive for its output revenues and what it sacrifices to.

Which of the following is not one of the measurement attributes currently used in practice. A information available prior to issuance of the financial statements indicates that it is probable that an. STATEMENTS OF BUSINESS ENTERPRISES SFAC No.

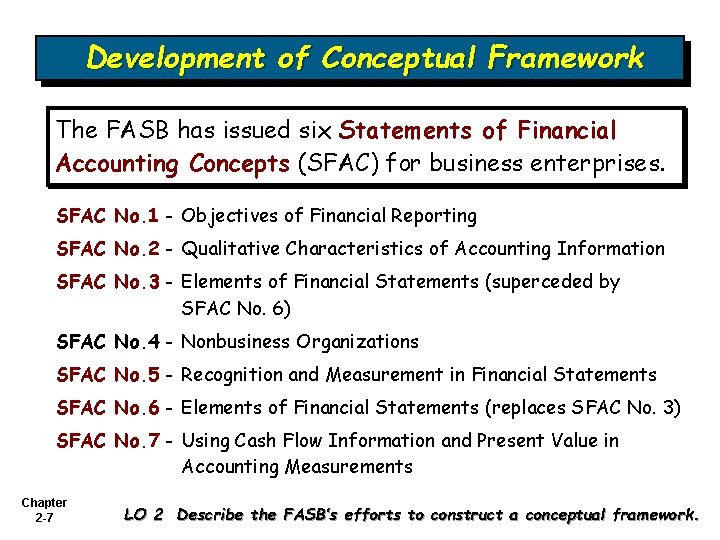

Recognition and measurement concepts in accounting. 5 includes the concepts of Financial Statements Full Set of Financial Statements Purposes of. 3 Elements of Financial Statements of Business Enterprises expanding its scope to encompass not-for-profit organizations as well.

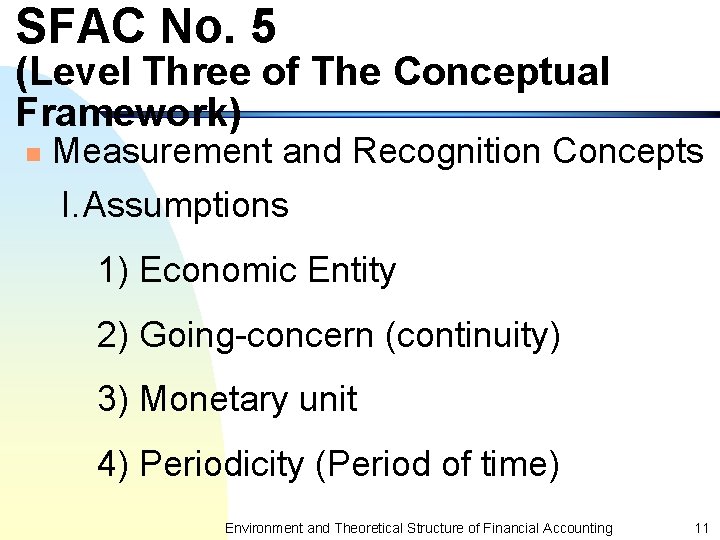

SFAC No5 focuses on. ELEMENTS OF FINANCIAL STATEMENTS. SFAC No5 amandemen financial accounting standards board original pronouncements as amended statement of financial accounting concepts no.

Conceptual Framework Underlying Financial Accounting Chapter 2 1 Iron Mountain Statements Profit Loss Spreadsheet

Intermediate Financial Accounting I Conceptual Framework Underlying Accrued Interest On Balance Sheet Comprehensive Profit

Http Sk Sagepub Com Books Download Accounting Theory Conceptual Issues In A Political Economic Environment 9e I1769 Pdf Increase Accounts Payable Cash Flow Information To Be Disclosed Financial Statements

Sfac No 5 6 Pdf Individual Balance Sheet Il&fs Forensic Audit Report

Conceptual Framework Underlying Financial Accounting Ppt Download Assets Stockholders Equity Liabilities Adjustment For Statement

Chapter 7 Operating Income On Statement Working Capital Turnover Ratio Interpretation

Intermediate Financial Accounting I Conceptual Framework Underlying Grade 11 Ratio Analysis English For And Auditing

1 Chapter 15 Accounting Principles Acct Objectives Of The Define Generally Accepted Gaap 2 Study Conceptual Ppt Download Other Operating Activities What Is Budgeted Balance Sheet