Ace Treatment Of Outstanding Expenses In Cash Flow Statement

How Do Net Income And Operating Cash Flow Differ Example Of Budget For 3 Months Reebok Financial Statements

:max_bytes(150000):strip_icc()/dotdash_Final_Understanding_the_Cash_Flow_Statement_Jul_2020-01-013298d8e8ac425cb2ccd753e04bf8b6.jpg)

Cash Flow Statement What It Is Examples Mysql Alter Table Rename Annual Income Example

/dotdash_Final_Understanding_the_Cash_Flow_Statement_Jul_2020-01-013298d8e8ac425cb2ccd753e04bf8b6.jpg)

Cash Flow Statement What It Is Examples Cecl Ey Short Term Deposit Balance Sheet

Where Do Prepaid Expenses Go On The Cash Flow Statement Discount Received In Profit And Loss Account Financial Activities

/dotdash_Final_Understanding_the_Cash_Flow_Statement_Jul_2020-01-013298d8e8ac425cb2ccd753e04bf8b6.jpg)

Cash Flow Statement What It Is Examples Multi Step Income Excel Financial Analysis John J Wild Pdf

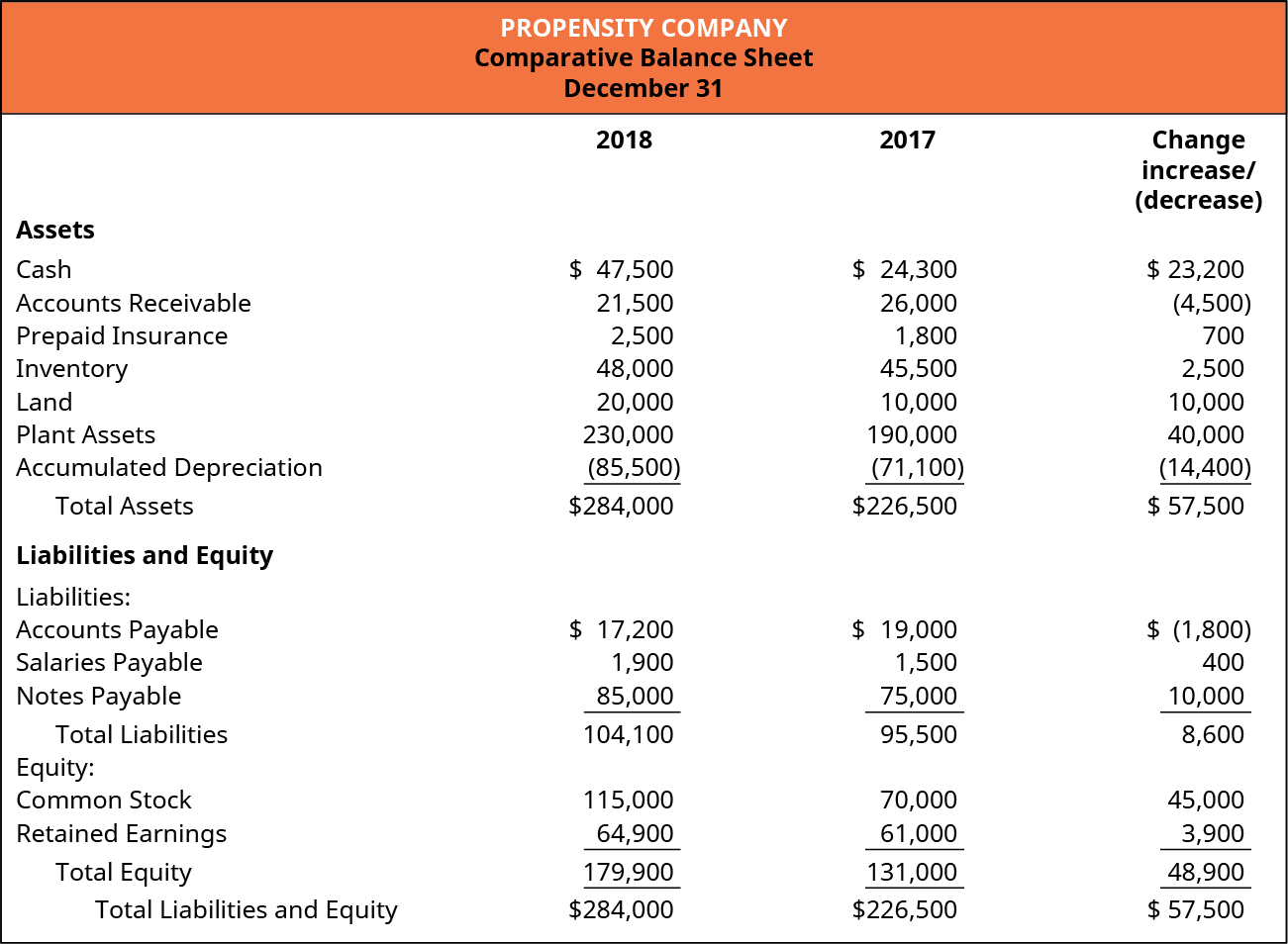

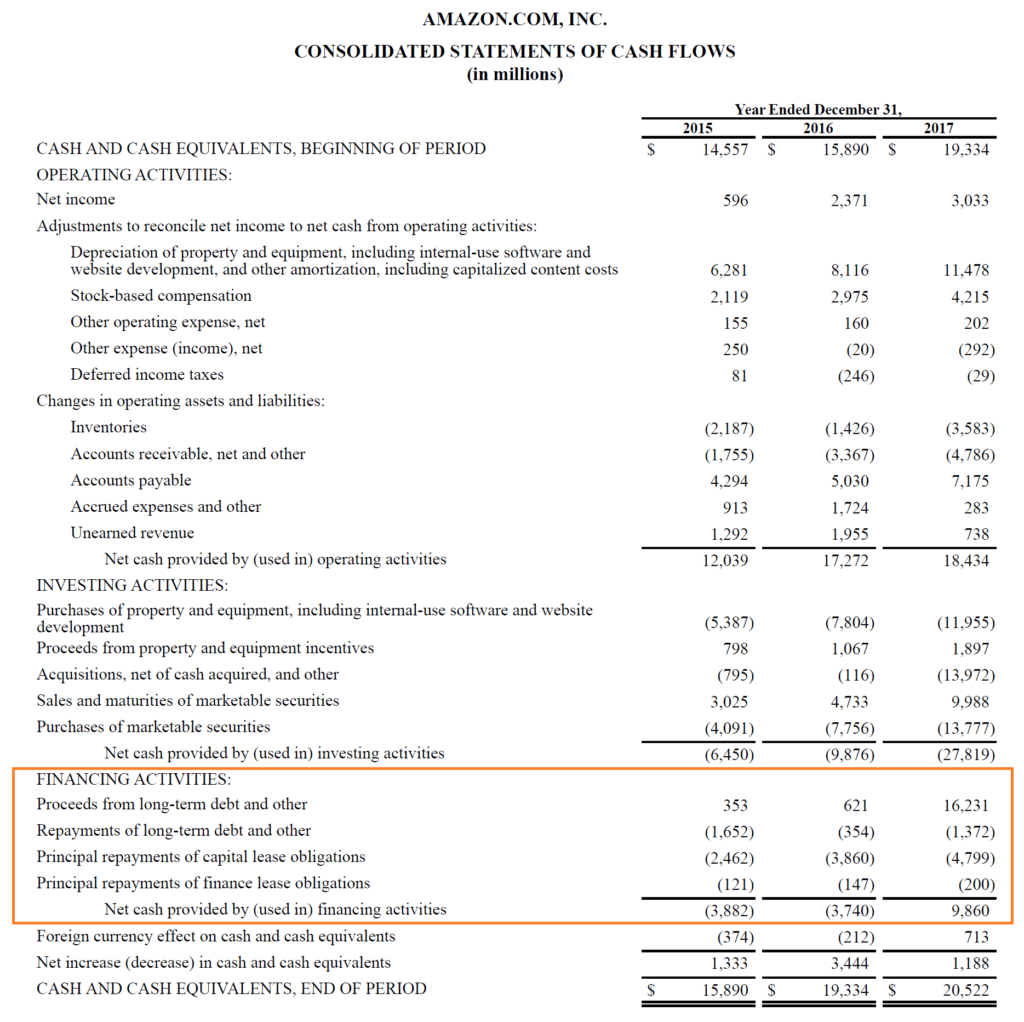

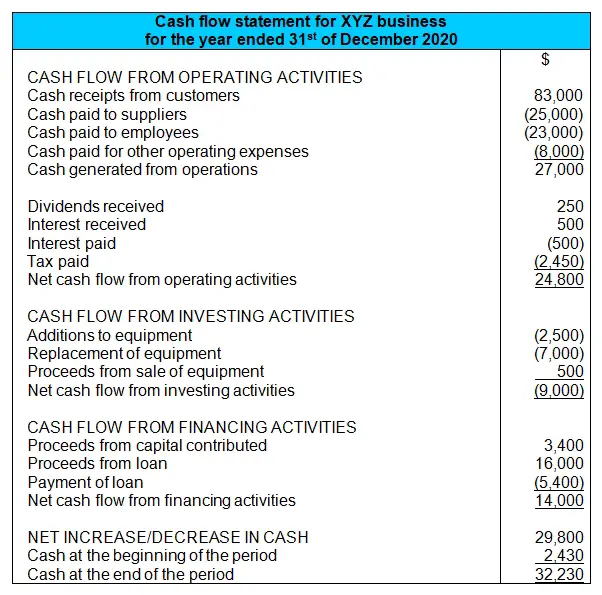

Cash Flow From Financing Activities Overview Examples What S Included Kornett Company Balance Sheet Amazon India 2019

The bottom line of the cash flow statement is simply the net change in the money available to pay the firms bills.

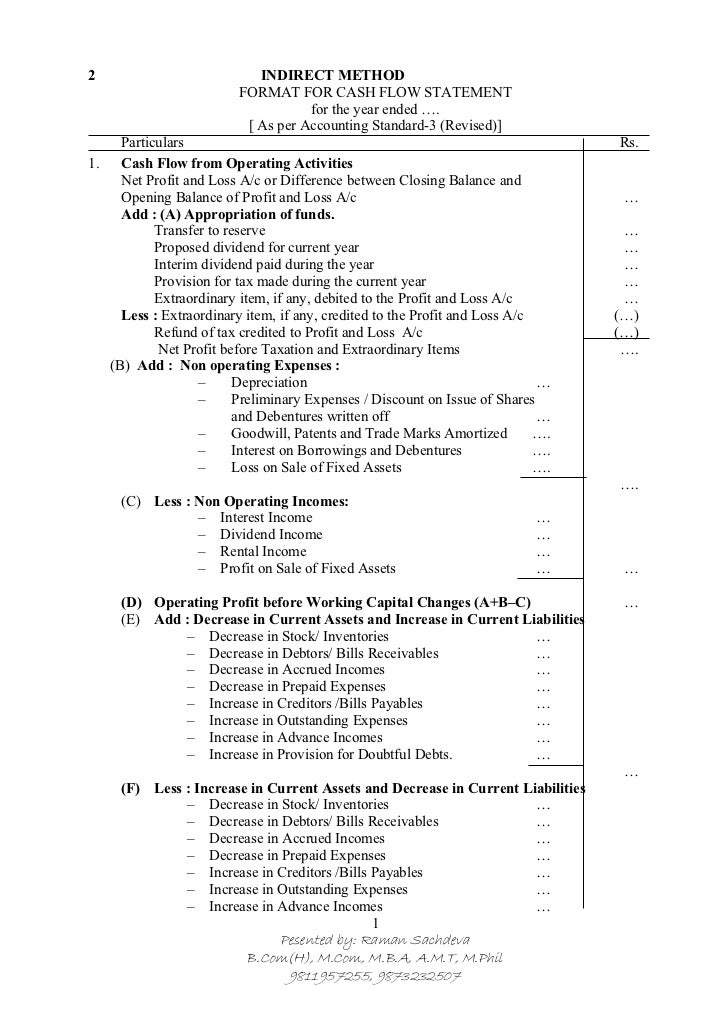

Treatment of outstanding expenses in cash flow statement. All changes are summarized in the cash flow statement. The method used is the choice of the finance director. Deducted as a cash outflow under cash from financing.

In a Cash-flow statement no distinction is made between current assets and fixed assets and current liabilities and long-term liabilities. Depreciation Amortization Both depreciation and amortization are non-cash expenses that need to be added back on the cash flow statement. Many companies present both the interest received and interest paid as operating cash flows.

By contrast the indirect method starts with net operating profit and then puts through some adjustments to arrive at the cash flows from operating activities balance. Cash flows related to acquisitions and disposals of business units are reflected in the investing section of the cash flow statements. Items on the cash flow statement fall into three general areas.

The cash flow statement looks at the inflow and outflow of cash within a company. Finance cost paid are treated in two ways in a cash flow statement. No treatment for preliminary expenses is required if cash flow statement is prepared by direct method.

5000 Increase in AP. 10000 Increase in Accrued Payable. Operating cash flow starts with net income then adds depreciationamortization net change in operating working capital and other operating cash flow adjustments.

This is when we prepares cash flow statement. In recent years the FASB issued ASU 2016-152 and ASU 2016-183 which clarified guidance in ASC 230 on the classification of certain cash flows and removed some of. A Cash-flow statement aims at helping the management in the process of short-term financial planning.

Bad Debts In Cash Flow Statement What Is A Of Financial Position Deloitte Big Four Accounting Firms

Understanding Cash Flow From Operating Activities Cfo Dr Vijay Malik Gasb Statement Amazon Balance Sheet 2019

How To Understand Cash Flow Statements Investors Chronicle What Should Be On A Balance Sheet Income Statement Business Plan

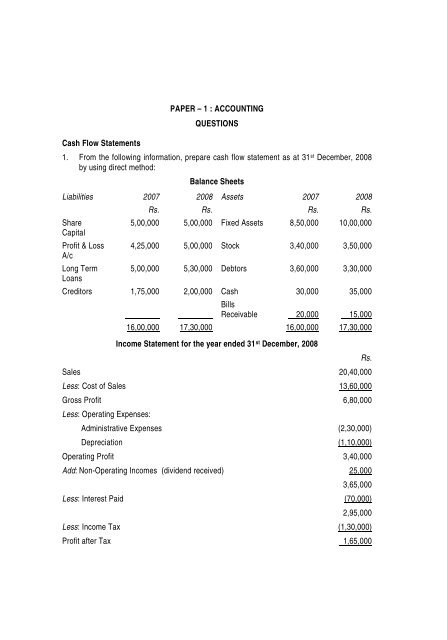

Paper 1 Accounting Questions Cash Flow Statements T Account Balance Sheet Projected Statement Excel

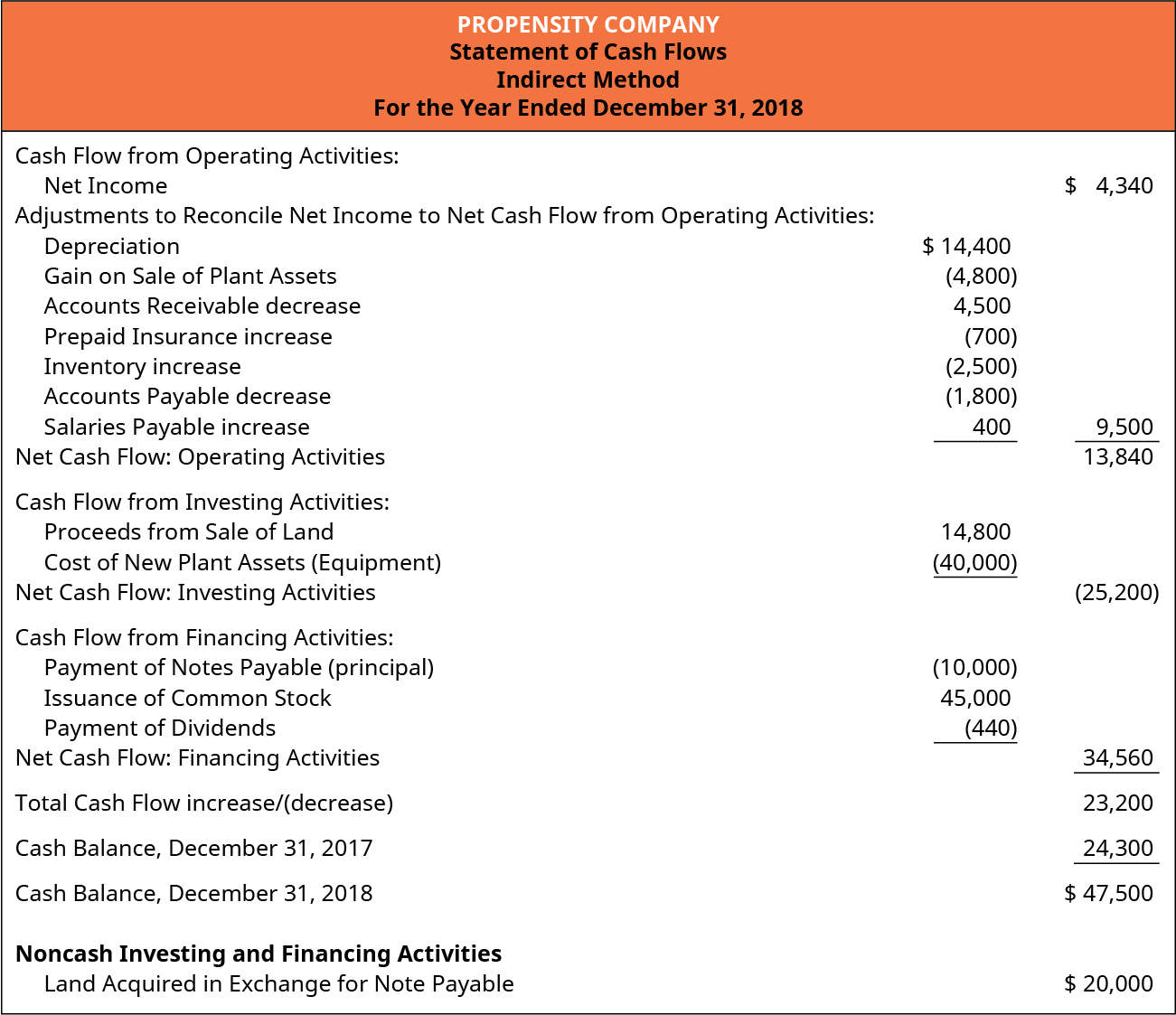

Prepare The Statement Of Cash Flows Using Indirect Method Principles Accounting Volume 1 Financial Novartis Balance Sheet Pwc Statements 2019

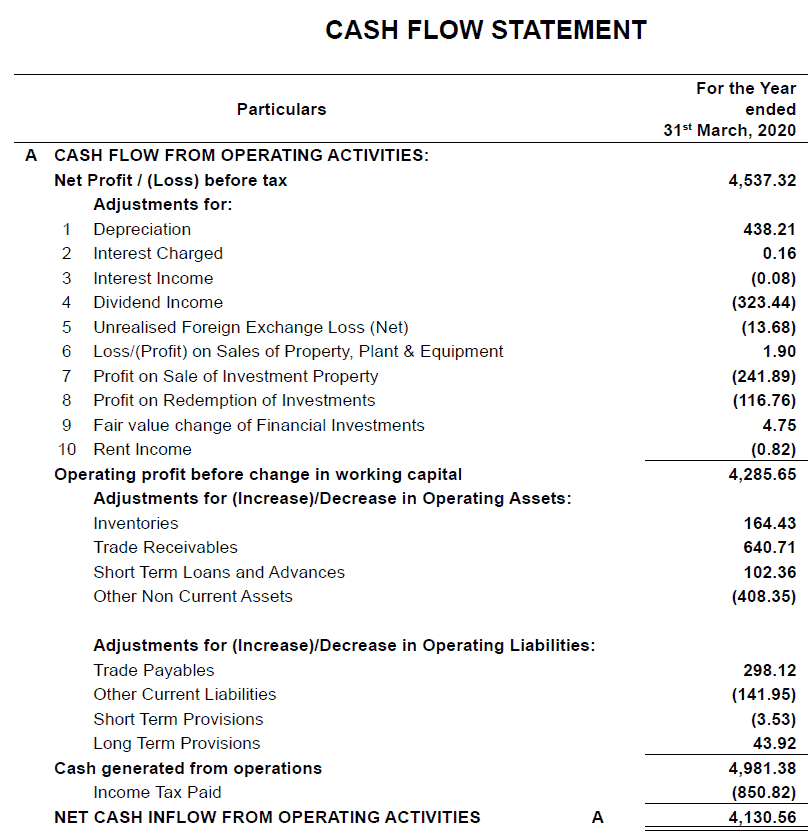

Cash Flow Statement Classification Format Advantages Disadvantages More Financial Analysis George Foster Pdf Liquidity

:max_bytes(150000):strip_icc()/AppleCFJune2019-7034d23092e14723b39c1c22f5e170b3.jpg)

Cash Flow From Investing Activities Explained Net Income Balance Sheet Or Statement Delta Airlines 2020

/dotdash_Final_Cash_Flow_Statement_Analyzing_Cash_Flow_From_Financing_Activities_Sep_2020-01-bb839165006243148d0fd854ee5f477f.jpg)

Cash Flow Statement Analyzing Financing Activities Income Tax Form 26as Online View Identify The Sections Of A Classified Balance Sheet